Market size, mill innovation, regulatory change, color direction, and sourcing risk, the intelligence colored denim professionals need heading into 2026 and beyond.

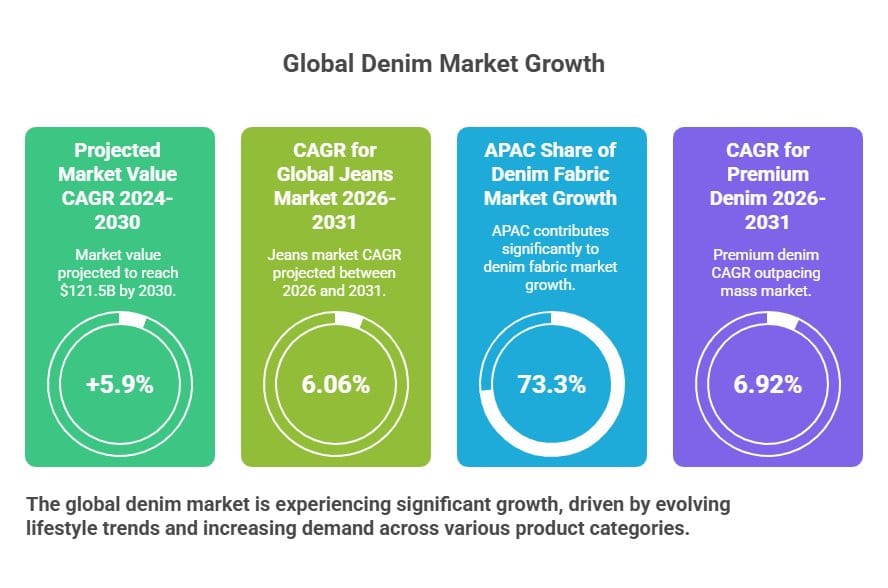

- The market is growing fast: The global denim market is forecast to reach $121.5 billion by 2030 at 5.9% CAGR. Colored denim’s share within this is rising as consumers actively seek non-indigo options across premium and mass segments.

- Mills are investing heavily in colored fabric innovation: Sulfur-bottom color innovations, new pigment and disperse dyeing capability, GRS-certified recycled color yarns, and expanded non-indigo color ranges are coming out of major mills for F/W 2026-2027.

- Regulation is changing your sourcing obligations: The EU Digital Product Passport for textiles is expected to require compliance by 2027-2030. The ban on destruction of unsold goods takes effect mid-2026 for large companies. These changes hit dye chemistry documentation hardest.

- Cotton price and supply risk is real: Global cotton production is contracting 2% in the 2025-2026 season. Prices are forecast to rise 2.9% in 2026 and again in 2027. Non-cotton fiber blends offer one mitigation route, particularly relevant for colored denim applications.

Colored denim is no longer a seasonal accent category. It is a structural growth area within a global denim market that is expanding faster than most adjacent apparel segments.

Non-indigo denim now spans a wide range of end-uses, price points, and technical specifications, and the mills supplying it are investing accordingly.

For designers, buyers, and sourcing professionals, the colored denim category in 2026 sits at the intersection of three active pressures.

These are accelerating consumer demand for non-blue options, a significant wave of fabric and process innovation from leading mills, and a regulatory environment that is reshaping what supply chain transparency means in practice.

This article consolidates the market intelligence that matters most to industry professionals working with or sourcing colored denim fabric in 2026 and planning for 2027.

The Global Denim Market: What the Numbers Show

The denim market is in a genuine growth cycle. That growth is being driven by casual lifestyle trends, the return of denim to semi-formal settings, a resurgence of premium denim demand, and the broadening of what denim products include beyond traditional jeans.

Regional Breakdown for Buyers

North America continues to hold the largest revenue share at approximately 31-32%, driven by strong brand presence and consistent per-capita denim consumption.

The average American owns approximately seven pairs of jeans, and replacement-driven purchasing keeps baseline volumes stable.

Europe is growing at 6.0% CAGR through 2030, driven by premium positioning, sustainability requirements, and the influence of major fashion events and retail innovation. European buyers are notably more active in the premium and eco-certified colored denim categories.

Asia-Pacific is the fastest-growing region and the manufacturing center. It contributes over 73% of incremental denim fabric market growth and accounts for roughly half of global denim manufacturing capacity.

China alone produces over 3 billion meters of denim fabric annually.[4]

The Premiumisation Driver

The premium denim segment is growing faster than mass market across every major region. At 6.92% CAGR through 2031, it outpaces the overall market by approximately one percentage point.

This is directly relevant to colored denim sourcing. Premium consumers are more willing to pay for non-indigo colors and more likely to purchase multiple colored denim pieces per year.

They are also more receptive to brands that can articulate the material and process story behind their products. Colored denim at premium price points commands higher margin and benefits from less price-sensitivity than equivalent mass-market volume.

Where Colored Denim Fits in the Market

Colored denim does not have its own cleanly separated market category in most industry research.

It sits within the broader denim market as a fabric type, competing for shelf space and consumer attention against the dominant indigo blue segment.

What is measurable is consumer direction. Market research consistently shows brands across segments are expanding their non-indigo offerings in direct response to demand for differentiation. The data points that matter most to buyers and product developers are these:

- Approximately 44% of denim brands have introduced sustainable or eco-focused collections, many of which feature non-indigo colors where low-impact dye processes are highlighted as a marketing differentiator.[5]

- The premium segment, where non-indigo color commands the most viable margin, is the fastest-growing denim category globally.

- Women’s denim is growing at 7.92% CAGR through 2031, the highest of any end-user segment. Women’s denim has historically shown greater openness to colored options than men’s, and seasonal color variations drive purchase frequency beyond replacement-only cycles.

- The dresses and tops categories are the fastest-growing denim product segments, both of which show higher colored denim adoption than traditional jeans.

The Differentiation Pressure

“There is too much denim that lacks differentiation,” Cristina Cerdeira of Tejidos Royo told WWD in early 2026. This view is shared across the supply chain.Buyers building distinctive collections increasingly turn to non-indigo color as one of the fastest ways to differentiate at the fabric level without new construction investment.

For sourcing professionals, this creates both an opportunity and a sourcing complexity.

The opportunity is in accessing an expanding range of colored denim fabric from mills investing heavily in this space. The complexity is in navigating dye chemistry documentation, color consistency at scale, and the new regulatory data requirements that attach to colored denim specifically.

Color Intelligence: What’s Moving in 2026 and 2027

Translating consumer trend data into denim fabric sourcing decisions requires understanding the specific color directions that are gaining enough commercial traction to justify ordering minimums and development investment.

The 2025-2026 Color Direction from Cotton Incorporated

Cotton Incorporated’s trend team has tracked a clear post-pandemic shift away from the saturated brights of the early 2020s.

Their 2025-2026 forecast identifies muted, powdery, chalky aesthetics as the dominant direction for colored denim.

This is being executed in fabric through special washes and yarn construction choices. Extreme washes on fabrics with sulfur black yarn in the warp and indigo weft produce a sun-bleached effect that reads as a colored finish.

Pigment-dyed cotton dobby stripes, overdyed with a secondary color, create layered neutral tones that sit between traditional colored denim and blue denim.

Metallic effects are also tracking forward. Cotton Incorporated has observed metallic denim achieved through foil printing and yarn construction for several seasons; for 2025-2026, these are evolving toward more futuristic aesthetics with gold foil on cotton denim providing antique finishes and clear polyurethane coatings delivering high-shine laminated effects.

WGSN and Runway-Level Color Signals

WGSN senior denim strategist Susie Draffan flagged 80s influences and colorful denim in the Spring/Summer 2026 collections as an early signal of a maximalist direction building for the next two seasons.

Opulent gold, tracked by WGSN as a key 2026 trend driver, is appearing in denim through coatings and metallic construction rather than dye alone.

The broader runway color picture for 2026 is a tension between vibrant electric shades (violet, scarlet, emerald at designer level) and the quieter palette anchored by Pantone’s 2026 Color of the Year, Cloud Dancer.

For buyers, this dual market means developing both a capsule of statement colored pieces and a broader range of washed-back neutrals.

The Commercial Color Picture for 2026

| Color Direction | Market Signal Strength | Key End-Use | Dye System | Sourcing Notes |

|---|---|---|---|---|

| Brown / Chocolate | Very strong, confirmed across multiple markets | Jeans, jackets, dresses | Sulfur or piece-dyed | High commercial confidence; order depth warranted |

| Earth tones (tan, khaki) | Strong, building since 2023 | Jeans, workwear-inspired pieces | Sulfur or reactive | Reliable for 2+ seasons; safe development investment |

| Muted / chalky pastels | Moderate, strong in premium | Women’s tops, dresses, jeans | Reactive dye + wash treatment | More season-sensitive; keep development capsules small |

| Metallic / foil effects | Moderate, runway to commercial lag | Premium occasionwear, denim accessories | Coating / foil print | Small run, high-margin positioning; test before scaling |

| Electric / vibrant brights | Early stage, designer-level only | Statement pieces, capsules | Reactive dye | Not yet commercial at scale; monitor for 2027 forward |

| Black (with effects) | Perennial, strong across all segments | All garment types | Sulfur black | Perennial investment; focus on wash differentiation |

| White / light wash | Strong, seasonal reliability | Spring/summer across all segments | Bleached or undyed cotton | High-volume reliability; invest in wash development |

Buyer’s note on color timing: Denim color trends move more slowly than most fashion categories. A shade with confirmed commercial traction typically holds for two to three seasons. Brown and earth tones have been building for three seasons, suggesting viability through at least end of 2027, a longer window than most seasonal color trends justify.

What Mills Are Producing: The Innovation Landscape

The most useful indicator of where the colored denim market is heading is what leading mills are developing for their F/W 2026-2027 collections and beyond. The following developments are drawn from direct industry reporting and mill announcements.

Developing sulfur-bottom fabrics in non-traditional shades including orange, jade, and warm browns to create distinct casts and tones. New machinery enabling pigment and disperse dyeing is expanding their capability to dye polyester and plastic-based fiber blends in colored denim constructions. Actively refining processes through test trials to introduce new color innovations at commercial scale.[6]

The Prism collection features nine colors from dark to light, blending nostalgic references with contemporary styling. The range is positioned as a versatility play for brands seeking to offer heritage-feeling colored denim without the complexity of custom color development. Multiple shades in a single coordinated collection simplifies buyers’ decision-making at the sampling stage.

Over 40 patented technologies developed in the past two years. Bigbox dyeing reduces water usage by up to 95% by consolidating traditional 8-13 dyeing boxes into a single unit. The Blue Loop Indigo Recovery System achieves 98% recovery rates for both water and unused dye. FitSense Denim and FreeCross Bi-Stretch represent innovations in performance-colored denim.[7]

The Forged range responds to demand for heavyweight, authentic fabrics with enhanced sustainability credentials. The mill also produces GRS-certified recycled content fabrics with colored thread woven in, offering a sustainable colored aesthetic without piece-dyeing.

In 2024, AGI Denim (affiliated) produced over 30 million meters of fabric incorporating recycled cotton, with nearly all clients now requiring recycled content.[8]

The Natural Comfort family delivers 100% cotton fabric with comfort-level stretch and 20% recycled cotton content, available across a range of colored finishes. At 10-15oz washed weight, with 15-20% stretch performance and no synthetic fibers, the fabrics are positioned as fully recyclable at end of life, a key specification for brands building DPP-compliant collections.

Chenille denim constructions (cotton indigo warp, polyester weft) available in sulfur and reactive dye options. The collection covers casual, lounge, and fashion applications with check and striped constructions and flocking detail options. Sulfur and reactive dye availability in the same construction range gives buyers flexibility in depth of color and wash-down performance.

Tencel lyocell HV100, launched in 2025, reads visually closer to cotton through variable fiber length cutting. Tencel 2.2 offers a denser, coarser hand positioned as a price-stable alternative to linen.

Both fibers take color differently from cotton, producing softer, more muted effects with lower dye uptake – relevant for brands targeting sustainable color narratives.[9]

Meadowsweet mid-weight fabric positions as a gender-neutral base suitable for jeans, fashion, dresses, and outerwear across multiple washes and dye treatments. The versatility of a single base fabric across multiple end-uses lowers development cost for brands building colored denim capsules. Dyed with Cone’s Distilled Indigo, which uses less water and resources than conventional powder dyestuffs.

What These Mill Developments Mean for Buyers

Several clear patterns emerge from this landscape.

First, the capability for colored denim is expanding beyond traditional reactive and sulfur-dyed piece goods. Mills are now offering sulfur-bottom color constructions that create tonal complexity through the interplay of dye types at yarn level.

This gives buyers more technical options for creating colored denim that behaves differently from standard piece-dyed fabric.

Second, the integration of recycled content into colored denim is moving from a premium niche to standard practice. Nearly all major mills in the supplier landscape now offer recycled cotton content options, and brands are increasingly specifying it as a baseline requirement rather than an optional upgrade.

Third, AI and digital tools are entering the mill-level development process. The Kingpins Show reported in early 2026 that many exhibitors are using AI in design assistance, trend tracking, raw materials modeling, and assortment planning, though the application remains in early-stage exploration rather than systematic deployment.[10]

Fiber Innovation and Its Effect on Color Performance

One of the most significant changes in colored denim development is the expanding range of fiber options available.

Cotton remains the dominant raw material, but blending with alternative fibers is now standard practice. Each alternative fiber creates a different color performance profile.

Why Fiber Choice Affects Color Output

Different fibers accept dye in fundamentally different ways. Cotton’s cellulose structure bonds well with reactive and vat dyes but poorly with disperse dyes used for polyester.

Lyocell (Tencel) accepts reactive dyes but produces softer, more muted color than cotton at equivalent concentrations. Wool blended into denim weft takes acid dye and produces a natural color variation that creates visual texture at the fabric surface.

For buyers sourcing colored denim, the same color specification applied to different fiber compositions will produce different results.

Understanding the fiber profile of a fabric is a prerequisite to predicting how a color will read on the final garment.

Key Fibers Reshaping Colored Denim in 2026

| Fiber | Color Effect | Sustainability Profile | Key Sourcing Consideration |

|---|---|---|---|

| Recycled cotton | Naturally muted and varied; can bypass some dyeing steps | Significantly lower water and chemical use versus virgin | Consistency of color output varies with recycled feedstock; specify acceptable variation range |

| Lyocell (Tencel) | Softer, more luminous color; lower dye uptake than cotton | Biodegradable; closed-loop production process | Price premium over cotton; verify DPP compatibility of supply chain documentation |

| Hemp | Earthy, organic-looking color with natural variation | Low water use; no pesticide requirement; soil-positive | Limited commercial scale; sourcing partnerships require advance planning |

| Linen / linen blends | Natural variation creates visual texture; muted color register | Lower water use than cotton; biodegradable | Price volatility; Lenzing Tencel 2.2 positioned as stable alternative |

| Wool blends | Rich, deep color with natural surface variation; requires separate dye system | Biodegradable; renewable; depends heavily on farming practice | Separate dye bath required for wool component; adds process complexity and cost |

| Organic cotton | Same color output as standard cotton; verified cleaner processing | Lower pesticide load; GOTS-certifiable | 46% of denim brands now sourcing organic cotton; supply is expanding but still price-premium |

From the industry: Textile expert Tricia Carey explained the appeal of alternative fibers in denim this way: “Denim’s coarser yarn counts make it more forgiving for fibers that may not be optimized for quality. Additionally, weft innovation provides opportunities to incorporate fibers that may not have the strength in warp applications since they don’t require dyeing.” For colored denim specifically, weft fibers that carry color differently from the indigo or sulfur-dyed warp create layered visual effects that cannot be achieved through dyeing alone.[8]

The Regulatory Compliance Imperative

The regulatory environment affecting denim sourcing is changing faster than at any point in the past decade.

For professionals sourcing colored denim specifically, the implications are particularly concentrated in dye chemistry documentation and product data requirements.

What follows is a timeline of the most operationally relevant regulatory developments, with direct implications for colored denim sourcing decisions.

EU ban on destruction of unsold goods takes effect for large companies. The ESPR regulation prohibits companies from destroying unsold consumer apparel and footwear. Crucially, recycling is classified as destruction under this rule. Brands must route excess inventory to resale, repair, or donation rather than disposal. This fundamentally changes how colored denim collections are planned, ordered, and managed at end of season. Overstocking carries new legal and reputational risk.

California Climate Accountability Package enforcement begins. Scope 3 reporting and supply chain due diligence requirements for companies operating in California, regardless of headquarter location. For denim brands with US retail operations, this means documented evidence of supply chain emissions including dyeing and finishing processes.[11]

EU ESPR Delegated Act for textiles expected. This act will set the specific rules for Digital Product Passports in the clothing and textile sector. Once adopted, brands will have an 18-month compliance window to implement DPP infrastructure. The DPP must contain fiber composition, chemical compliance data, environmental footprint, origin, and end-of-life guidance. For colored denim, the dye chemistry documentation requirement will be the most operationally demanding element.[12]

EU Digital Product Passport mandatory for textiles. Full DPP compliance required for all textiles sold in EU markets by 2030. A Bain and eBay report suggests DPPs could effectively double the lifetime value of fashion products by enabling more trusted and efficient resale, rental, and repair markets. Early adopters gain both compliance security and new commercial channels.

France’s mandatory eco-score expected mid-2026. All producers, importers, or distributors of clothing and home textiles sold in France must calculate and display an aggregated environmental impact score covering GHG emissions, water use, and biodiversity. Applicable to all companies selling in France regardless of origin. Colored denim’s dyeing water use will directly affect this score.[13]

What This Means Specifically for Colored Denim Sourcing

The DPP requirement will be more demanding for colored denim than for blue indigo denim. Non-indigo dye systems use a wider range of chemical inputs.

Reactive dyes, sulfur dyes, pigment systems, and specialty coatings each have distinct chemical compliance profiles under REACH and OEKO-TEX frameworks.

Documenting dye chemistry at a product level requires data from Tier 3 and Tier 4 suppliers, the dye manufacturer and chemical supplier level, that most brands do not currently collect as standard. Building those data relationships now, before DPP requirements are enforced, creates a meaningful compliance advantage over competitors who wait.

Action now: Do not wait for the delegated act to begin auditing your colored denim dye chemistry data. The 18-month compliance window from the expected late 2026/early 2027 delegated act means brands that have not started supply chain data collection by mid-2026 will be in a compliance scramble. Begin mapping Tier 3 and Tier 4 supplier relationships for your non-indigo denim lines this season.

Market Risks: What Could Disrupt Growth

The denim market growth projections are credible, but they are not guaranteed. Industry professionals need to plan around the risks that could slow or complicate the colored denim growth trajectory.

| Risk Factor | Severity | Likelihood | Mitigation |

|---|---|---|---|

| Cotton price inflation | HIGH | HIGH, forecast 2.9% rise 2026, again 2027 | Blend strategy with recycled cotton, lyocell, or linen; forward buying where viable |

| Cotton supply contraction | MODERATE | HIGH, 2% global production decline expected 2025-2026 | Diversify fiber sourcing; increase recycled cotton content; expand MMCF options |

| Tariff exposure | HIGH | MODERATE, Kontoor reported $15M impact in 2025 | Nearshoring strategy review; manufacturing geography diversification |

| DPP compliance cost burden | MODERATE | HIGH, regulatory timelines confirmed | Early investment in supply chain traceability infrastructure; data partnerships with key mills |

| Reactive dye consistency at scale | MODERATE | MODERATE | Specify acceptable color deviation ranges; require QC protocol documentation from mills |

| Consumer demand slowdown | MODERATE | LOW-MODERATE | Colored denim premiumization shields margins better than volume market; focus on justified price points |

| Greenwashing regulatory exposure | HIGH for reputation | MODERATE | Third-party certification for all sustainability claims; ensure dye chemistry documentation supports claims |

The Cotton Price Risk in Detail

Cotton price risk deserves specific attention because it affects colored denim more acutely than blue denim.

Non-indigo colors often require more processing steps, higher dye cost, and more water-intensive finishing. These costs are already embedded in a higher fabric price point than standard indigo denim.

When cotton prices rise, the cost base for colored denim inflates at multiple points: raw fiber, yarn spinning, and the more expensive dyeing processes.

Brands without sufficient retail margin face a choice between absorbing the increase or re-pricing at a level that may suppress demand in price-sensitive segments.

The World Bank’s forecast projects cotton at $1.75 per kilogram in 2026 (up 2.9% from 2025) and $1.80 in 2027.[14] Sourcing strategies built around recycled cotton or alternative fiber blends offer the most direct mitigation, alongside a review of minimum order quantities and development capsule sizing.

Sourcing Colored Denim: A Practical Framework

For buyers and product developers building or expanding colored denim programs, the following framework covers the key decisions and data requirements at each stage of the sourcing process.

Define your color program scope before approaching mills. Know whether you are building a perennial colored denim program (year-round colors that carry across seasons) or seasonal capsule additions (trend-driven colors with a single-season window). This determines your minimum order strategy, color fastness specification requirements, and mill partnership depth. Perennial programs warrant deeper mill relationships and more stringent color consistency requirements.

Specify dye chemistry requirements as part of your brief, not after sampling. Ask mills to confirm which dye system will be used for each color at brief stage. Sulfur dyes, reactive dyes, and pigment systems produce different color profiles, different wash-down behaviors, and different environmental documentation requirements. Knowing the dye system up front avoids technical surprises at lab dip stage.

Require full Tier 3 chemical supplier documentation for DPP preparation. For any brand selling in the EU, the DPP will require dye and chemical ingredient data. Mills that can provide this data now are significantly more valuable sourcing partners than those who cannot. Build this requirement into your supplier assessment criteria.

Specify a color deviation acceptance range in writing. Reactive dyes used for bright colored denim have higher batch-to-batch variation than indigo. Define your acceptable Lab Delta E tolerance in writing before production begins. Standard industry practice is Delta E less than 1.5 for commercial production; tighter specifications may be warranted for premium or print-adjacent programs.

Verify sustainable process claims against certifications, not marketing language. Ask specifically for GOTS, Bluesign, or OEKO-TEX Standard 100 documentation for the colored fabric, not for the mill’s broader production. A mill may have Bluesign certification for its indigo production while using conventional chemistry for reactive-dyed colored fabrics. Request certificate scope documentation.

Build inventory management for the EU unsold goods ban into your buying strategy now. The mid-2026 prohibition on destruction of unsold goods applies to products placed on the EU market. Colored denim capsule programs carry higher unsold inventory risk than perennial blue denim. Plan resale routes, take-back partnerships, or B2B clearance channels for colored stock before buying, not after.

The Fabric Cost Comparison Calculator helps you evaluate total cost of ownership across different denim fabric specifications, including sustainable alternatives.

What to Ask Mills: A Sourcing Checklist

These are the questions that professional buyers should be able to answer before placing a colored denim production order:

- What dye system is used for this color? Is it sulfur, reactive, pigment, or a combination?

- What is the dye fixation rate, and what percentage of applied dye enters wastewater?

- Is the fabric GOTS, Bluesign, or OEKO-TEX Standard 100 certified? What is the scope of that certification?

- What is the water consumption per linear meter for this fabric including dyeing and finishing?

- Can the mill provide Tier 3 chemical supplier documentation for DPP compliance purposes?

- What is the minimum order quantity, and what color deviation tolerance is the mill able to hold commercially?

- What wash-down performance should be expected after 10, 20, and 50 domestic wash cycles?

- Does the fabric contain elastane or other synthetic content that would restrict end-of-life recyclability?

For more on how different colored denim types perform across care and use cycles, the complete colored denim fabric guide provides detailed fabric-level specifications useful for product development briefing.

For small brands and independent designers applying many of these same decisions at lower volumes, the sourcing and working with colored denim guide covers the operational detail — MOQs, fabric testing, supplier briefing, and labeling requirements — from a small-scale perspective.

Frequently Asked Questions

What is the current market size for colored denim fabric specifically?

Colored denim does not have a cleanly separated published market size, as industry research typically covers the broader denim fabric and denim jeans categories. The overall denim jeans market was valued at approximately $86.7 billion in 2024 and is projected to reach $121.5 billion by 2030 at a 5.9% CAGR. Colored denim’s share within this is growing, driven by premiumisation trends, women’s denim growth (7.92% CAGR), and expanding denim product categories beyond jeans including dresses, which show higher colored adoption rates.

Which dye system is most commercially reliable for colored denim production at scale?

Sulfur dyes are the most commercially reliable system for dark colored denim including black, dark grey, and deep brown, due to established process infrastructure and lower per-unit cost. Reactive dyes offer the widest color palette for mid and bright tones but require careful batch consistency tolerances.

For buyers prioritising long-term color stability and established mill capability, sulfur-dyed dark colors represent lower production risk than reactive-dyed brights at equivalent order volumes.

What does the EU Digital Product Passport mean for colored denim sourcing now?

The DPP for textiles is expected to become mandatory between 2027 and 2030, with the delegated act for textiles anticipated in late 2026 or early 2027. Once adopted, brands have approximately 18 months to comply.

For colored denim, the DPP will require documentation of dye chemistry and chemical compliance at a product level. Brands should begin mapping Tier 3 and Tier 4 supplier relationships for non-indigo dye inputs now, before the compliance window opens.

How is cotton price volatility affecting colored denim development budgets?

Cotton prices are forecast to rise 2.9% in 2026 and again in 2027 as global production contracts. Colored denim is more exposed than standard blue denim because non-indigo dyeing already carries higher per-unit cost.

Sourcing strategies blending recycled cotton, lyocell, or alternative fibers offer the most direct mitigation. Development budgets for colored programs should build in a 5-8% raw material cost buffer for the 2026-2027 planning horizon.

What colors are showing the strongest commercial traction for colored denim buyers in 2026?

Brown and earth tones (tan, khaki, terracotta) have confirmed commercial traction across multiple markets and are expected to hold through at least end of 2027. They represent the safest development investment for non-indigo programs.

Muted and chalky pastels are performing in premium women’s segments. Metallic effects are moving from runway to premium retail. Electric brights remain at designer-level only and are not yet commercially viable at standard buying volumes.

What should buyers specify in mill briefs to ensure DPP-ready colored denim?

At minimum, your mill brief for DPP-ready colored denim should request the dye system used, the name of the dye manufacturer and specific dye products, REACH compliance status for all dye inputs, and water consumption data per linear meter.

Also request OEKO-TEX or Bluesign certification scope documentation specific to the colored fabric. Mills that cannot provide this data are not viable DPP partners regardless of price or relationship history.

How does the EU ban on destruction of unsold goods affect colored denim buying strategy?

The mid-2026 ban on destruction of unsold apparel and footwear (for large companies) fundamentally changes how end-of-season colored denim stock must be managed. Recycling counts as destruction under this rule, meaning unsold colored stock must be routed to resale, donation, or repair. Colored denim capsule programs carry higher unsold inventory risk than perennial blue denim. Buyers should plan resale routes and B2B clearance partnerships before buying seasonal colored programs, not as an afterthought when stock does not sell through.

What is the significance of the premiumisation trend for colored denim margins?

The premium denim segment is growing at 6.92% CAGR through 2031, outpacing the mass market. Premium consumers are more willing to pay for non-indigo colors and purchase more frequently, especially in women’s segments.

Brands able to articulate color origin, dye process, and material composition at product level command meaningful price premiums. The DPP infrastructure will eventually standardize and make these claims verifiable, strengthening the margin case further.

Conclusion

The colored denim market is growing from a position of genuine commercial strength. The underlying fundamentals, a $86.7 billion market expanding at nearly 6% annually, premiumisation driving the highest growth, women’s and non-jeans categories expanding fastest, all favor a well-executed colored denim program.

The challenge for industry professionals is that this growth opportunity arrives simultaneously with the most significant regulatory compliance shift the denim industry has faced in a generation. The EU Digital Product Passport, the ban on destruction of unsold goods, CSRD reporting requirements, and France’s mandatory eco-score all land within a two-to-three-year window that starts now.

For colored denim specifically, regulatory complexity is higher than for blue denim because non-indigo dye chemistry involves more chemical inputs, more complex wastewater profiles, and less established documentation infrastructure in mill supply chains.

The key operational priorities for 2026:

- Focus colored denim development investment on commercially confirmed shades, brown, earth tones, white, dark washes, rather than chasing trend-level early signals like electric brights.

- Begin Tier 3 and Tier 4 supplier data mapping for non-indigo dye inputs now, before DPP compliance requirements are enforced.

- Build cotton price volatility into your colored denim development budgets for 2026 and 2027. Factor in 5-8% raw material cost buffer, or pivot development toward recycled cotton and alternative fiber blends.

- Plan EU unsold goods strategy before buying seasonal colored denim programs, not after. Resale and B2B clearance partnerships need to be in place before stock is ordered.

- Use mill capability in sustainable dyeing technology (foam dyeing, ozone finishing, closed-loop water systems) as a tier-1 selection criterion for colored denim sourcing, not a secondary consideration.

- The brands and buyers that build DPP-compliant supply chains now gain a market access advantage in EU markets and a data infrastructure advantage for the broader transparency requirements that will follow globally.

The complete colored denim fabric guide provides the technical fabric-level specifications useful for product development briefing. For the full picture on sustainability implications specific to colored denim, the colored denim sustainability guide covers the environmental cost in detail.